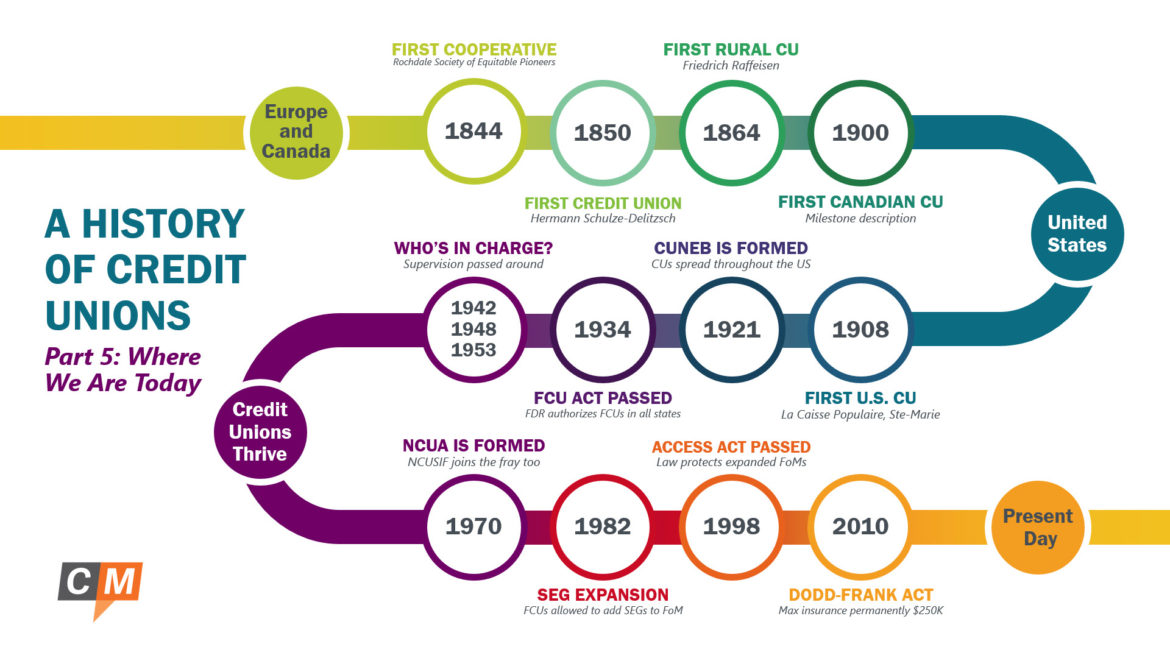

2008 – The Great Recession and the 2010 Dodd-Frank Act

2008 saw the greatest financial crisis the world had suffered since the Great Depression in the 1930s. Banks suffered considerably, and while credit unions would also suffer, the impact on the industry was relatively small compared with their larger counterparts.

To protect members, share insurance was temporarily increased from $100K to $250K in 2008. Then, as part of the Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010, a response to the crisis that made large, sweeping changes to financial regulation, that share insurance amount was made permanent.

In the wake of the crisis, disgruntled and disillusioned Americans flocked to credit unions which had suffered far less. The non-for-profit and cooperative nature of the industry appealed to a population frustrated with Wall Street. Activists organized Bank Transfer Day on November 5, 2011 encouraging people to move their funds and business to credit unions. An estimated 440,000 new memberships and $4.5 billion in funds were moved over.

Credit unions have a long and storied past filled with a passion for serving their communities. More than 100 years after the first credit union in America opened its doors, credit unions are still going strong, but are not without their own challenges. Although members and total assets are at an all time high, consolidation and emerging competition continue to threaten the industry. All the same, the passion for the industry is as high as ever–where there’s a need for financial services, there are those willing to help, and that’s where credit unions will continue to best serve.

Whew! I hope you enjoyed this history of credit union series. If there’s some major milestone that you felt was missed, let me know in the comments.