Financial Literacy Month is back and it’s time to spend a little time learning about how credit unions and the wider financial industry work!

Here at CUSO Magazine, we publish a good deal of content on the things credit unions are doing to spread financial literacy among their members, and offer advice on how to reach your membership to improve their financial well being. But what about credit union leaders’ financial literacy?

There is no shame in admitting that we may each have blind spots in terms of our own understanding of how the credit union industry works. And so some years ago I set out to bridge the gap of my own ignorance and pass along what I learned to our readers.

Ordinarily, these articles have a heavy focus on credit unions, from the ratios executives use, to how to read a financial statement, explaining corporate credit unions, and figuring out how to balance net worth (among others!). Today, however, I am going to widen the net of financial literacy and focus on the financial markets and how they impact credit union operations.

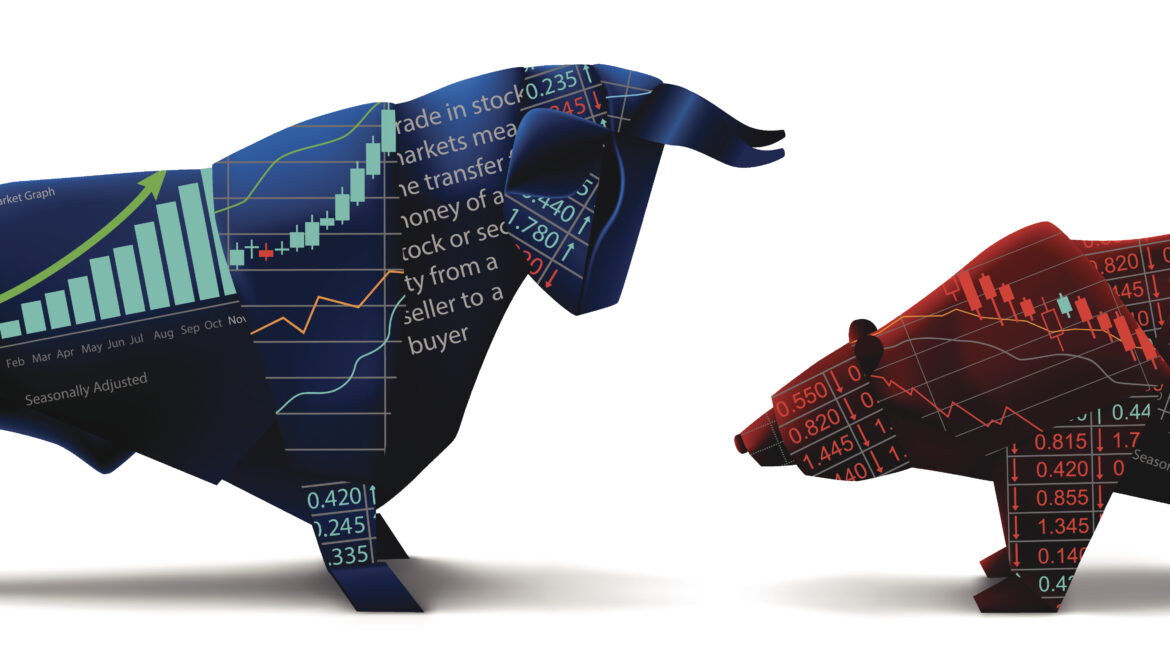

“Bear” and “Bull” markets

Before getting into the nitty-gritty of how the markets directly or indirectly affect credit unions, let’s first get an understanding of some used and playful (but not always harmless) terms: bear and bull markets.

Both terms are used to indicate dramatic market trends, in opposite directions of one another. Where a bull market is a positive trend, with a steady increase in the price of stocks, a bear market is characterized by a steep drop in consumer confidence and stock prices. In order for downturn to be considered a “true” bear market, the markets must see a 20% drop from recent highs.

Another way to look at it is that in a bull market, demand for securities is strong as people feel confident that prices will increase, but sellers are fewer, resulting in prices rising. Alternatively, in a bear market, confidence is low, driving securities holders to seek to offload their portfolios; but as demand is low and supply is high, the price will be driven down, further exacerbating the fears of a collapsing market.

If you are anything like me, you may have some familiarity with the two terms, but confuse the two as they do not seem particularly intuitive. One easy way to remember which is which is that a bull will swipe up with its horns (rising market), whereas a bear will swipe down with its claws (declining market).

The use of “bull” and “bear” to describe markets—and not just stock markets—dates back to at least the late 19th century and possibly even earlier. Though there is some disagreement as to each term’s origin, one possible origin for the use of bear to denote a negative trend is from the proverb suggesting it is unwise to “sell the bear’s skin before one has caught the bear.” Going back yet further finds some uses of the term “bear-skin jobber” to denote an individual who’s selling something that does not exist. Over time, the use of bear to denote a market in decline could then refer to those speculating on the market’s demise before it has happened, becoming a self-fulfilling prophecy.

An early use of the term “bull” to refer to somebody who’s anticipating higher prices on securities can be found in the 1769 edition of the book Every Man his own Broker, which refers to bulls as those who would buy government securities on credit, hoping that they could pocket the profit on a future gain.

As bull markets tend to span many years, such as in the years leading up to the dotcom bubble, they get less attention than the catastrophic and often accelerated bear markets, such as the market crash of 1929, the Great Recession in 2009, and the collapse in the wake of the pandemic in 2020.

Credit unions are built to weather market volatility

Now that we have an understanding of bear (bad) and bull (good) markets, let’s take a look at how credit unions can be affected by market volatility.

As member-owned institutions, credit unions differ from banks in their profit-seeking motivations. A successful credit union will pass its success on back to its owners in the form of lower rates, better access to financial tools and services, and even return of profits back in the form of patronage dividends.

The Great Recession started as the result of unsound investment strategies from banks and lenders seeking to capitalize on the housing market. According to a report by the Financial Crisis Inquiry Commission in 2011, banks were approving mortgages that would prove to be a bad credit risk. As the housing market boomed, lenders then began bundling those mortgages and selling them as mortgage-backed securities, which investors believed to be otherwise safe.

However, as the tide began to turn and defaults rose, the value of those securities and associated derivative products plummeted. As banks and investors lost money hand over fist, it resulted in a credit crunch. The eventual collapse of Bear Stearns and Lehman Brothers would tip the scales into the disastrous. In all, over 450 FDIC-insured banks failed between 2008 to 2012.

Alternatively, credit unions were able to weather the storm more favorably. From January 2008 through June 2011, 5 corporates and 85 credit unions failed. The corporates, in particular, were hit hard due to their own investment in mortgage-backed securities.

In general, though, as credit unions have more stringent risk management requirements, they were less directly impacted. Those that failed were in many cases the results of the havoc on the market at large, including members affected by an economic downturn and resulting defaults.

In 2008, credit unions were already subject to the CAMEL rating, which assesses a credit union’s risk profile on five measures: capital adequacy, asset quality, management, earnings, and liquidity. In 2022, the NCUA added an ‘S’ to the end for sensitivity to market risk, which you can read about in my previous financial literacy article.

Should the market face another potential recession (as news outlet after news outlet has speculated on for months), credit union members can feel confident that the credit union industry will weather it with aplomb.

I hope you have enjoyed this look at bear and bull markets and how they impact credit unions. Next week, I will dive into the confusing world of cryptocurrency and blockchain.